Market Insights 6/15/26

Observations & Insights – June 15, 2026

Cars & Coffee is this coming Saturday

10am to Noon in the Asbury Wealth N. Parking Lot

https://www.facebook.com/groups/1209913187155887

Markets Cut a Jagged Path

The 0.7% returns that the S&P 500, NASDAQ, and Dow each posted for the week did not come easily, as stocks sold off on Wednesday before rebounding on Thursday and Friday. The modest overall results left the indexes below the record levels recorded in the first few days of June.

Key Points

- Stock markets rebounded slightly after a volatile week.

- While volatility is elevated, the pullback in mega-cap stocks is normal bull market behavior.

- High oil prices continue to drive inflation, but that is not the whole story.

- The much-anticipated Space-X IPO came to market on Friday, capturing investors’ imaginations and capital.

Observations: Inflation Stays Elevated, Europe Raises Rates

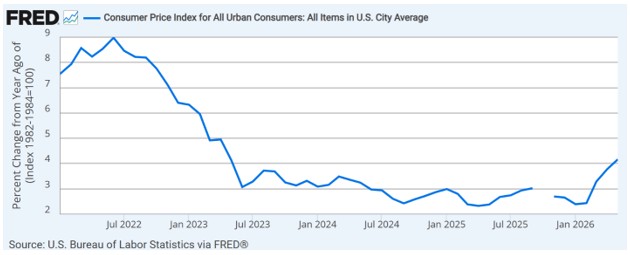

The Consumer Price Index (CPI) report showed inflation running at 4.2% in May, the highest level in more than three years. Despite the rise in the annual rate, the month-to-month change eased slightly compared with April’s CPI figure, and inflation readings for non-energy categories were relatively stable. A separate report on wholesale prices showed a 6.5% annual rate for the Producer Price Index, the highest since November 2022.

A U.S. small-cap stock index outpaced its large-cap peers by a wide margin, climbing to a record high and extending small caps’ year-to-date performance leadership. The Russell 2000 Index finished around 4% higher for the week and was up 19% year to date.

The European Central Bank raised its benchmark interest rate for the first time since 2023, lifted its inflation forecast, and downgraded its economic growth outlook. In announcing Thursday’s widely expected quarter-point rate hike, ECB policymakers cited inflationary pressures, elevated energy prices, and the Middle East conflict.

Oil prices continued to take cues from developments in the Middle East, with U.S. crude jumping more than 3% on Wednesday, only to fall on Friday afternoon to the lowest level since mid-April. Oil climbed above $93 per barrel on Wednesday and was trading around $84 on Friday afternoon, down about 6% for the week.

An indicator that tracks investors’ expectations of short-term U.S. stock market volatility traded in a wide range, reflecting shifts in the outlook for the Middle East conflict. On Wednesday, the CBOE Volatility Index closed at the highest level since April 7; by Friday’s close, however, the VIX was trading nearly 18% below the previous week’s closing level.

A monthly gauge of U.S. consumer sentiment improved, snapping a string of three consecutive monthly declines amid elevated energy prices. The University of Michigan’s survey results released on Friday showed that sentiment rose to a preliminary June reading of 48.9 from a final May figure of 44.8.

The two-day U.S. Federal Reserve meeting that’s scheduled to conclude on Wednesday will be the first session led by Kevin Warsh, who’s taking over as Fed chair after his nomination cleared Congress last month. While the Fed is expected to keep interest rates unchanged, Warsh’s post-meeting news conference and an updated policy statement could offer clues about current market expectations for a potential rate hike by year end.

Insights: Five Things to Reflect On

“It is human nature to overestimate risk and underestimate opportunity.” Jeff Bezos

Here are a couple things I have been thinking about lately.

Bad Days Happen

Last Friday, the S&P 500 fell by -2.6%, marking the worst day of the year. Yes, it did not feel good, but after the historic nine-week rally, it would have been foolish not to expect some type of give-back. Something to know, is even the best years have bad days. In fact, we found that 22 years gained at least 20% in a given year, and the average worst-day return was a loss of 3.5%. In fact, there was a day in 1997 when the S&P 500 tanked nearly 7%, yet stocks still gained more than 30% that year. Volitility happens.

Source: FactSet

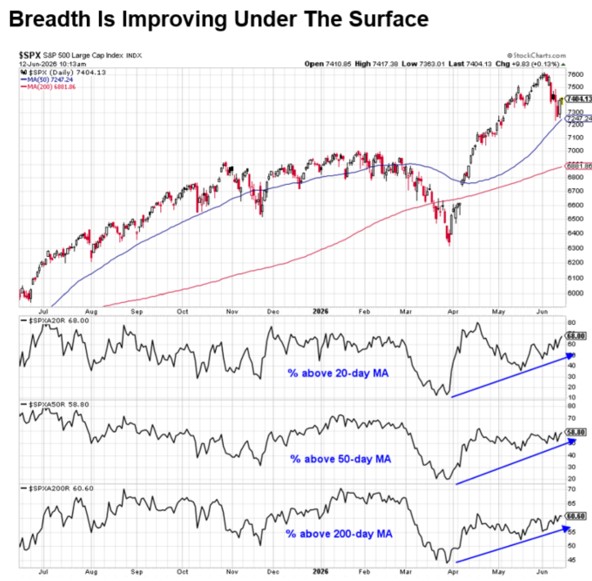

Breadth Is Holding Up Well

Yes, technology has been taking a well-deserved break, but other areas and sectors are holding up quite well. In fact, on Tuesday, the S&P 500 fell, yet advancing stocks outnumbered the declining stocks by a 2-to-1 ratio, an extremely rare development.

I am encouraged that the number of stocks in the S&P 500 above their 20-day, 50-day, and 200-day moving averages has all been increasing recently, even as the overall market index price has weakened. This is a clue that things are not falling apart; under the surface, things are doing well, as market participants rotate from one sector to the next.

Source: StockCharts

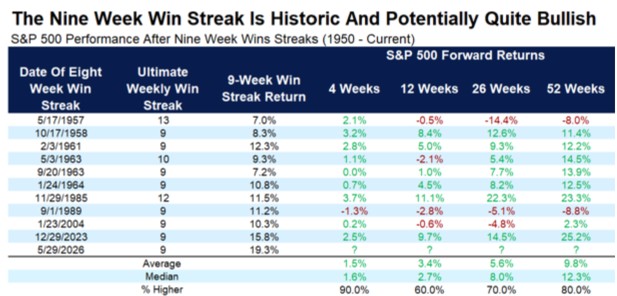

About That Nine-Week Win Streak

Yes, the S&P 500’s nine-week win streak ended recently. And maybe you would expect forward returns after such a strong run to give back a little. But historically, that is just not the case. After a nine-week streak or longer ends, the S&P 500 is higher a year later 80% of the time with an average gain of 9.8%. That is only about average for all periods, but it is important to remember that “average” historically is solidly bullish.

Source: FactSet

This is also the strongest nine-week return we have ever seen to start a streak of nine weeks or longer. Streaks with stronger returns have tended to mean a better follow-up in the next 52 weeks, with the S&P 500 averaging over 20% in the 52 weeks following the prior top three nine-week win streak returns (2023, 1961, 1985).

Stocks Don’t Peak in June

The most recent all-time high was on June 2 and pulled back a max -4.5% so far, but could this really be the peak for the year? We remain bullish, so we do not think so, but something to think about is that June is the only month in history that has never seen the ultimate peak for the year. Yes, most years peak either in January or December, which makes sense, but we do not think this year will be the first one to peak in June, and this is another positive for the bulls.

Source: FactSet

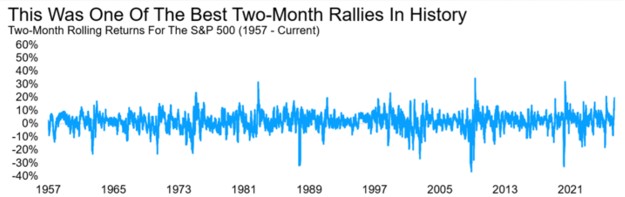

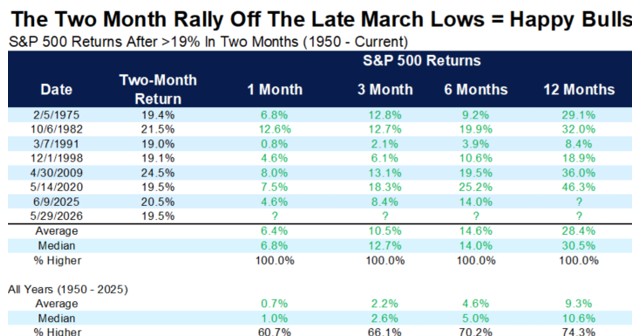

What A Two-Month Rally

Stocks soared for the two months off the late March lows, so some weakness in June is not a huge surprise. Here is a nice way to show this.

Source: FactSet

Putting more context around this, the S&P 500 gained 19.5% in only two months off the late March lows. This was one of the greatest two-month rallies in history, but previous large rallies were all quite bullish going forward.

We found only 7 other times in history when stocks gained more than 19% in 2 months, and in every case, they were higher 1-, 3-, 6-, and 12-months later, with a median return a year later of more than 30%.

Source: FactSet, Bloomberg

Final Thoughts: SpaceX (the IPO)

This week's market action was overshadowed by one of the most significant events in capital markets history: the public debut of SpaceX. The company completed the largest IPO ever, raising approximately $75 billion and achieving a valuation exceeding $2 trillion after a strong first day of trading. Demand was extraordinary, with both institutional and retail investors clamoring for shares, highlighting the continued appetite for innovation, technology, and long-duration growth opportunities.

For investors, the SpaceX IPO is about much more than rockets and satellites. It signals that capital markets remain healthy and willing to fund ambitious ideas despite ongoing concerns about interest rates, government deficits, and economic uncertainty. Many of the most transformative businesses of the past decade have remained private far longer than previous generations of companies, limiting public investors' access to their growth. The successful launch of SpaceX into the public markets could open the door for other highly anticipated private companies to follow. More broadly, the enthusiasm surrounding this offering reinforces a theme we have discussed often: investors continue to reward innovation, productivity, and technological leadership. While short-term volatility is always possible following a highly anticipated IPO, the broader message is one of confidence in American entrepreneurship, confidence in technological progress, and confidence that investors are still willing to look beyond today's headlines toward tomorrow's opportunities.

It is our aim at Asbury Wealth Partners that you find the market commentary we provide informative and useful. As our success grows mainly through referrals from our clients, we encourage you to share this weekly newsletter with your friends, family, and colleagues. If you are a client, we thank you for your business and your confidence. If you are not yet a client, we encourage you to contact us today and explore how our team may be able to add value to your unique financial situation.

Thanks as always for reading, and I hope everyone is off to a great start to summer!

Thank You,

Jeff

~~~~~~~~~~~~~~~~~~~~~~~

Jeffrey S. Markewich

Wealth Advisor

Off – 719-548-8103

Cell - 719-357-7747

Text – 702-493-9678

TF - 888-328-7655

~~~~~~~~~~~~~~~~~~~~~~~

An Introduction to Your Friends & Family

is the Greatest Compliment You Can Give

Jeffrey Markewich is a Registered Representative with, and securities and advisory services offered through LPL Financial, a registered investment advisor, Member FINRA/SIPC.

The information contained in this email message is being transmitted to and is intended for the use of only the individual(s) to whom it is addressed. If the reader

of this message is not the intended recipient, you are hereby advised that any dissemination, distribution or copying of this message is strictly prohibited. If you have received this message in error, please reply and you will be removed.

These views are those of the author, not of the broker-dealer or its affiliates. This material contains an assessment of the market and economic environment at a specific point in time and is not intended to be a forecast of future events, or a guarantee of future results. All investments involve risk, including loss of principal. Forward-looking statements are subject to certain risks and uncertainties. Actual results, performance, or achievements may differ materially from those expressed or implied. Information is based on data gathered from what we believe are reliable sources.

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual. All performance referenced is historical and is no guarantee of future results. All indices are unmanaged and may not be invested into directly.

The NASDAQ Composite Index measures all NASDAQ domestic and non-U.S. based common stocks listed on The NASDAQ Stock Market. The market value, the last sale price multiplied by total shares outstanding, is calculated throughout the trading day, and is related to the total value of the Index.

S&P 500 – A capitalization-weighted index of 500 stocks designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries.

The Dow Jones Industrial Average is comprised of 30 stocks that are major factors in their industries and widely held by individuals and institutional investors.

The Russell 2000 Index is an unmanaged index generally representative of the 2,000 smallest companies in the Russell 3000 index, which represents approximately 10% of the total market capitalization of the Russell 3000 Index.

The CBOE Volatility Index? (VIX?) is meant to be forward looking, showing the market's expectation of 30-day volatility in either direction, and is considered by many to be a barometer of investor sentiment and market volatility, commonly referred to as “Investor Fear Gauge”.

International investing involves special risks such as currency fluctuation and political instability and may not be suitable for all investors.

All indexes referenced are unmanaged. The volatility of indexes could be materially different from that of a client’s portfolio. Unmanaged index returns do not reflect fees, expenses, or sales charges. You cannot invest directly in an index. Consult your financial professional before making any investment decision.

There is no guarantee that a diversified portfolio will enhance overall returns or outperform a non-diversified portfolio. Diversification does not protect against market risk.

Asset allocation does not ensure a profit or protect against a loss.

The Consumer Price Indexes (CPI) program produces monthly data on changes in the prices paid by urban consumers for a representative basket of goods and services (Source: U.S. Department of Labor).

The Gross Domestic Product (GDP) is a comprehensive measure of U.S. economic activity. GDP measures the value of the final goods and services produced in the United States (without double counting the intermediate goods and services used up to produce them). Changes in GDP are the most popular indicator of the nation's overall economic health.

Government bonds and Treasury bills are guaranteed by the US government as to the timely payment of principal and interest and, if held to maturity, offer a fixed rate of return and fixed principal value.

LPL Tracking #1121474