Market Insights

Observations & Insights – June 8, 2026

Market Streak Snaps

The S&P 500 reversed course after nine consecutive weeks of gains, as a Friday sell-off in many semiconductor-related stocks weighed on the broader market. The index finished the week down about -2.5% overall, while the NASDAQ dropped -4.7% and the Dow slipped just -0.2%.

Key Points

- The stock market winning streak finally broke after nine consecutive weekly gains, one of the strongest periods in recent history.

- Market pullbacks are a normal part of investing but can be violent at times.

- Friday’s jobs report showed strength, despite rhetoric suggesting AI will supplant workers.

- The odds of an interest rate hike are increasing, with a strong jobs market, stubbornly high inflation and strong economic growth.

Observations: Jobs Strength Raises Rate Hike Odds

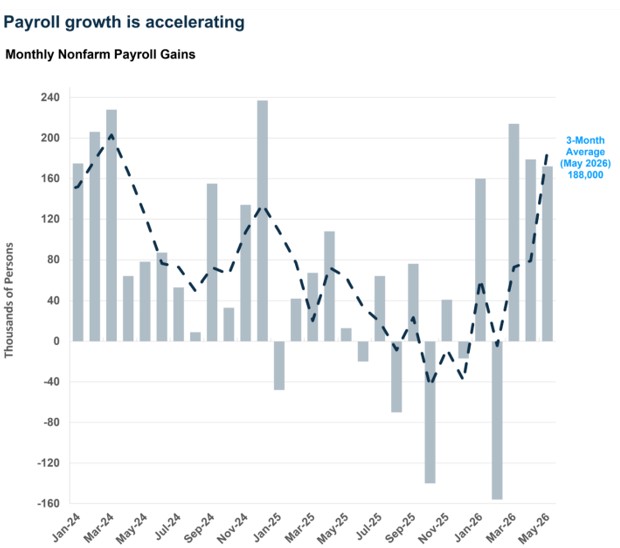

Recent labor market strengthening extended into May, as jobs growth surpassed economists’ consensus expectations for the third month in a row. The economy added 172,000 jobs, and upward revisions of prior estimates produced an average monthly gain of 188,000 jobs over the past three months. That is the strongest three-month average since March 2024.

A recent bond market sell-off regained momentum after a nearly two-week pause, as yields of U.S. government bonds rose in the wake of Friday’s better-than-expected jobs report. The steepest rise came at the short end of the yield curve, with the 2-year Treasury’s yield closing at 4.16% on Friday, well above the previous week’s closing yield of 4.00%.

Bond market trading reflected rising expectations for a U.S. interest rate increase by year end. Friday’s trading in rate futures markets implied a roughly 72% probability that the Fed would lift its benchmark rate by anywhere from a quarter-point to three-quarters of a point by December, according to CME FedWatch. The probability of rates remaining unchanged was 27%, with less than a 1% probability of a cut.

Bitcoin fell for the fourth week in a row as the price of the most widely traded cryptocurrency tumbled to the lowest level since September 2024. As of Friday afternoon, Bitcoin was trading around $60,000, down nearly 18% for the week. The cryptocurrency is well below a recent peak of around $82,000 reached on May 10 and a record high of $126,000 set last October.

Companies in the S&P 500 posted an average earnings gain of 28.6% over the same quarter a year earlier, according to FactSet data from the recently concluded first-quarter earnings season. That result marked the highest growth rate since the fourth quarter of 2021 and the sixth consecutive quarter of double-digit growth. Information technology posted a 54.0% earnings gain, the highest among all 11 sectors.

The latest developments in the Middle East conflict buffeted oil prices, as U.S. crude traded in a wide range, briefly climbing above $96 per barrel on Wednesday before settling to around $90 on Friday afternoon. For the week, oil was up nearly 4%.

The Consumer Price Index report scheduled for release on Wednesday will show whether a recent trend of rising inflation extended into June. The most recent CPI report showed an annual rate of 3.8% in April, the highest level since May 2023, with energy costs accounting for 40% of the increase from March’s 3.3% figure. Excluding energy and food prices, core inflation was 2.8% in April.

Insights: The Labor Market is Perfectly Fine

So much for the “AI is killing jobs” rehtoric, let alone “the Fed should keep rates low to protect the labor market”. We have been in the camp since the start of the year that the labor market looks better than a lot of economists, market bears, and even the good folks at the Fed may think. We even suggested the labor market may see some re-acceleration. Well, the data are bearing that out right now.

The May payroll report blew past expectations, with the economy adding 172,000 jobs, well above economists’ expectations of just 88,000. Moreover, payroll growth for March and April was revised up by a total of 93,000. That is a reminder that the initial estimate can vary widely, and why it is useful to focus on the 3-month average. The 3-month average of payroll gains is currently 188,000, the highest since March 2024. For perspective, the 3-month average was -39,000 at the end of 2025, and across all of last year, payroll growth averaged a measly 10,000 per month (116,000 jobs created over the full year). What else would you call that other than re-acceleration?

Source: FRED

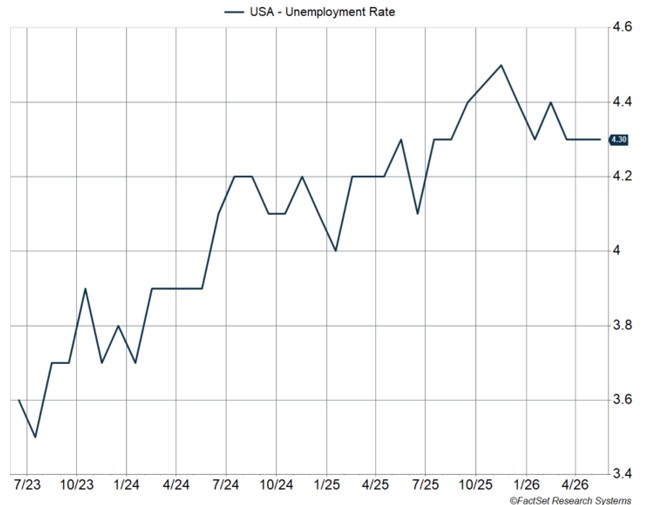

As noted above, payroll growth can and has been revised a lot in recent years, and that is why it is useful to corroborate what is happening with other data points. Notably, the unemployment rate comes from a household survey (payroll growth numbers come from a business survey). Well, the unemployment rate is sitting near historical lows at 4.3%. This should not be a huge surprise, given that payroll growth is clearly outrunning population growth (especially with immigration pulling back). There is no question that the labor market was weakening last year, with the unemployment rate rising from 4% to 4.5% between January and November, but we have clearly turned the corner now.

Source: FactSet

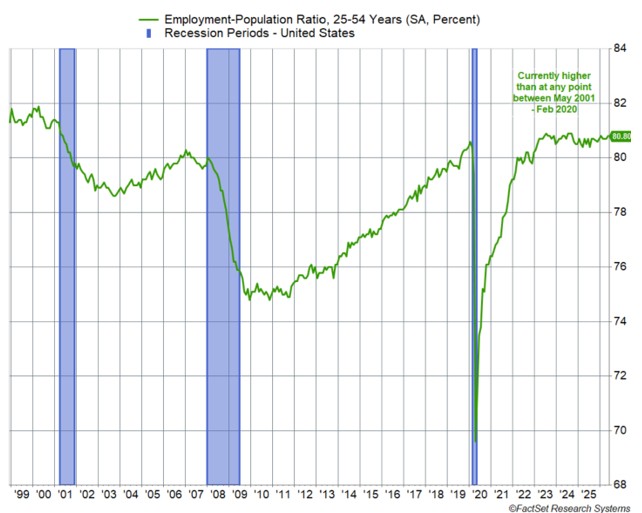

Better yet, the prime age (25-54) employment-population ratio rose to 80.8%, just shy of this cycle’s peak of 80.9% and higher than at any point between May 2001 and March 2023. In other words, more people in their prime working age years are employed today than at any point during the last two expansion cycles (relative to the age group’s population).

Source: FactSet

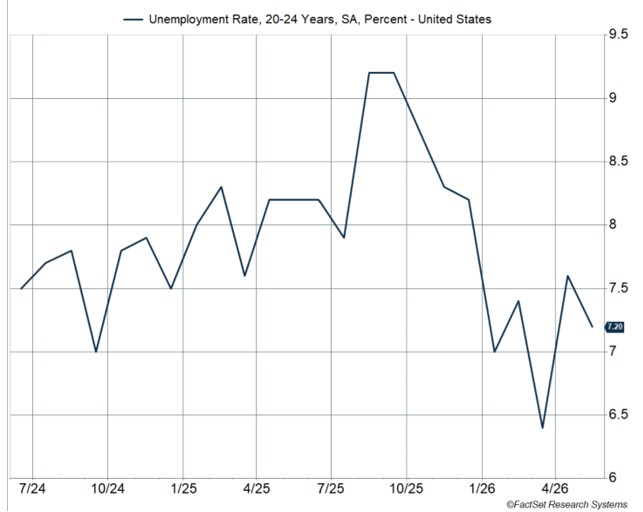

The prime-age employment-population ratio is useful because it gets around the fact that we have an aging population (so more people leave the labor force every day), and definitions around who is actually counted as “unemployed”, an unemployed worker who is “actively” looking for a job is counted as unemployed, but not someone who has given up after months of searching. The fact that the prime-age employment-population ratio is as high as it is goes against the prevailing narrative that “AI is taking away jobs.” That is not even the case for young people, whose job prospects AI would have a greater (adverse) impact on. Yet, for 20-24 year olds, the unemployment rate has fallen from 9.2% last September to 7.2% in May, even as AI implementation has grown.

Source: FactSet

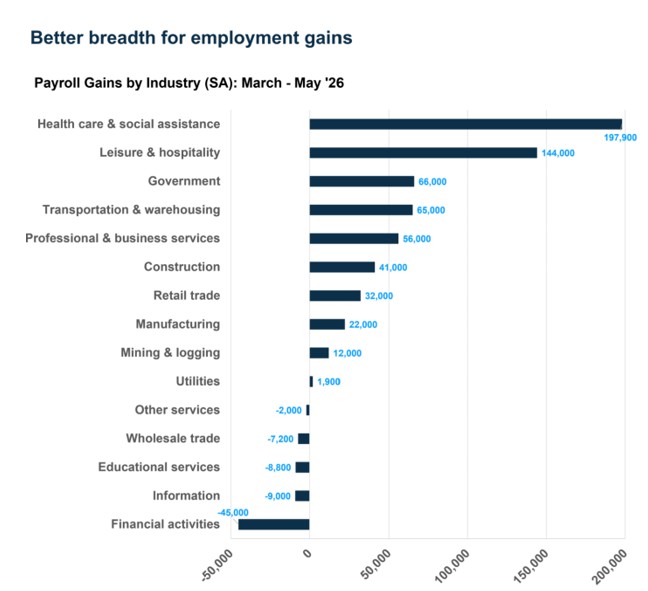

Better Employment Breadth

Things are even looking better under the hood. Over the past few years, employment gains within the health care sector have dominated job growth, while more cyclical areas of the economy lagged. This was especially the case in 2025, but that’s changed recently.

Over the past three months, payrolls have grown by 565,000. Health care payroll growth remains dominant, accounting for 35% of total payroll growth (198,000 jobs). But several cyclical areas are also showing up well, including leisure and hospitality (+144,000), transportation and warehousing (+65,000), professional and business services (+56,000), construction (+41,000), and even manufacturing (+22,000). The rebound in manufacturing is welcome, especially since manufacturing payrolls fell by 88,000 between February 2025 and February 2026.

Source: FRED

One prominent area where job growth is lagging is the tech industry. Payrolls across the telecommunications and data processing/hosting/related services industry have fallen by about 40,000 over the last year and have been flat recently. However, rather than AI replacing workers, it is more likely a result of companies laying off workers from over-hiring during COVID to free up capital budgets for AI-related infrastructure.

The Fed is Fiddling While Inflation Burns

The labor market looks strong right now, and inflation is heating up. As I have been pointing out for several months now, this is not just an energy problem because the Strait of Hormuz remains shut. The fact that the Strait remains shut is certainly a problem, and it is going to feed into non-energy inflation as well, via higher food prices and transportation costs. But we are also seeing elevated inflation due to AI-related bottlenecks, tariffs, and even core services (ex-housing) inflation. The personal consumption expenditures (PCE) index for core services is up 3.6% from last year and running at a 3% annualized pace over the last three months (through April). For perspective, the pace was just 2.2% in 2018-2019. The fact that services inflation is running hot has been a sign that the labor market is in better shape than headline numbers suggested up until a few months ago, i.e., there would not be upward price pressure on services if wage growth was weak and people were losing their jobs.

Source: FRED, Bloomberg

The fact that inflation is running hot and rising, while the Fed keeps interest rates unchanged, to me means policy is getting loose, possibly too loose. Normally, a backdrop of a relatively healthy labor market and elevated (and rising) inflation would have the Fed thinking about rate hikes. Instead, it looks like the Fed, especially under incoming Chair Kevin Warsh, will look past elevated inflation. This could be dangerous both economically and politically.

For now, an easier monetary policy is good news for the stock market. However, the problem grows behind the scenes. At some point, whether it is a year from now or 2-3 years from now, the Fed may realize that inflation has run too high for too long and will have to be even more aggressive to get inflation back to target. Policy rates should probably be about 0.5% to 1.0% higher than they are now.

To be clear, the inflation problem can hardly be laid at the Fed’s feet. The fiscal deficit is running around 6% of GDP, well above anything we have seen this deep into an economic expansion, usually as expansions wear on, the deficit gets smaller, but the opposite is happening now. With Congress and the administration asleep at the wheel, the job lands at the Fed to pull things back. But it does not look like a Warsh-led Fed is ready to tackle it; instead, it wants to move the inflation goalposts (including removing “outliers”) to keep policy easy and run things hot.

In my opinion, and the bond market is already reflecting this, there is clearly a cost, in the form of higher inflation and higher bond yields (which add to the federal government’s interest burden). Higher inflation means real (inflation-adjusted) wage growth is falling. Higher bond yields translate to higher borrowing costs across the economy, including higher mortgage rates, and that is shutting out an entire cohort of millennials from the housing market. Keep in mind that housing has historically been the primary vehicle for building wealth for middle-income households, but the entryway is now blocked by high mortgage rates.

Volatility Is the Price of Admission

This week's market action served as an important reminder that pullbacks are a normal and healthy part of investing. While headlines often make short-term market declines feel significant, history shows that stock market selloffs occur regularly, and sometimes violently, even during some of the strongest bull markets on record.

S&P 500 Pulls Back (1-week)

Source: Seeking Alpha

Which is Perfectly Normal in a Bull Market, S&P 500 (2026 to date)

Source: Seeking Alpha

Investors often forget that volatility is not a flaw of the stock market; it is the price we pay for the opportunity to earn higher long-term returns. Every meaningful bull market has experienced periods of uncertainty, profit-taking, and sharp short-term declines along the way. The path to long-term wealth creation has never been a straight line.

S&P 500 Volatility Index (VIX) 1-week

Source: Seeking Alpha

One of the biggest mistakes investors make is confusing volatility with risk. Volatility is temporary price movement. Risk is the permanent loss of capital. For disciplined investors focused on long-term goals, temporary market declines are often little more than noise within a much larger upward trend.

The current backdrop remains constructive. Corporate earnings continue to grow, economic activity remains resilient, and the Federal Reserve still appears positioned to keep policy accommodative. While markets will undoubtedly experience additional bouts of volatility, those periods should be expected rather than feared.

A useful perspective is that pullbacks are often the mechanism that keeps bull markets healthy. Excess optimism gets reset, speculative positions are reduced, and valuations become more attractive. In many cases, the strongest advances occur after periods of market discomfort.

As investors, our job is not to predict every short-term market move. Our job is to remain disciplined, focused on fundamentals, and committed to a long-term plan. Market volatility can be uncomfortable, but it is also entirely normal. The investors who are ultimately rewarded are usually the ones who stay invested when uncertainty feels the greatest.

Final Thoughts

The lesson from this week is simple: volatility is inevitable, but abandoning a sound investment strategy because of it is often far more damaging than the volatility itself. Bull markets do not climb in a straight line. They advance through a series of rallies, pauses, and pullbacks. Volatility is the fee investors pay for long-term wealth creation. This week's sell-off may have felt uncomfortable, but history suggests that temporary declines are often the toll road, not the roadblock, to long-term investment success.

It is our aim at Asbury Wealth Partners that you find the market commentary we provide informative and useful. As our success grows mainly through referrals from our clients, we encourage you to share this weekly newsletter with your friends, family, and colleagues. If you are a client, we thank you for your business and your confidence. If you are not yet a client, we encourage you to contact us today and explore how our team may be able to add value to your unique financial situation.

Thank You,

Jeff

~~~~~~~~~~~~~~~~~~~~~~~

Jeffrey S. Markewich

Wealth Advisor

Off – 719-548-8103

Cell - 719-357-7747

Text – 702-493-9678

TF - 888-328-7655

~~~~~~~~~~~~~~~~~~~~~~~

An Introduction to Your Friends & Family

is the Greatest Compliment You Can Give

Jeffrey Markewich is a Registered Representative with, and securities and advisory services offered through LPL Financial, a registered investment advisor, Member FINRA/SIPC.

The information contained in this email message is being transmitted to and is intended for the use of only the individual(s) to whom it is addressed. If the reader

of this message is not the intended recipient, you are hereby advised that any dissemination, distribution or copying of this message is strictly prohibited. If you have received this message in error, please reply and you will be removed.

These views are those of the author, not of the broker-dealer or its affiliates. This material contains an assessment of the market and economic environment at a specific point in time and is not intended to be a forecast of future events, or a guarantee of future results. All investments involve risk, including loss of principal. Forward-looking statements are subject to certain risks and uncertainties. Actual results, performance, or achievements may differ materially from those expressed or implied. Information is based on data gathered from what we believe are reliable sources.

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual. All performance referenced is historical and is no guarantee of future results. All indices are unmanaged and may not be invested into directly.

The NASDAQ Composite Index measures all NASDAQ domestic and non-U.S. based common stocks listed on The NASDAQ Stock Market. The market value, the last sale price multiplied by total shares outstanding, is calculated throughout the trading day, and is related to the total value of the Index.

S&P 500 – A capitalization-weighted index of 500 stocks designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries.

The Dow Jones Industrial Average is comprised of 30 stocks that are major factors in their industries and widely held by individuals and institutional investors.

The Russell 2000 Index is an unmanaged index generally representative of the 2,000 smallest companies in the Russell 3000 index, which represents approximately 10% of the total market capitalization of the Russell 3000 Index.

The CBOE Volatility Index? (VIX?) is meant to be forward looking, showing the market's expectation of 30-day volatility in either direction, and is considered by many to be a barometer of investor sentiment and market volatility, commonly referred to as “Investor Fear Gauge”.

International investing involves special risks such as currency fluctuation and political instability and may not be suitable for all investors.

All indexes referenced are unmanaged. The volatility of indexes could be materially different from that of a client’s portfolio. Unmanaged index returns do not reflect fees, expenses, or sales charges. You cannot invest directly in an index. Consult your financial professional before making any investment decision.

There is no guarantee that a diversified portfolio will enhance overall returns or outperform a non-diversified portfolio. Diversification does not protect against market risk.

Asset allocation does not ensure a profit or protect against a loss.

The Consumer Price Indexes (CPI) program produces monthly data on changes in the prices paid by urban consumers for a representative basket of goods and services (Source: U.S. Department of Labor).

The Gross Domestic Product (GDP) is a comprehensive measure of U.S. economic activity. GDP measures the value of the final goods and services produced in the United States (without double counting the intermediate goods and services used up to produce them). Changes in GDP are the most popular indicator of the nation's overall economic health.

Government bonds and Treasury bills are guaranteed by the US government as to the timely payment of principal and interest and, if held to maturity, offer a fixed rate of return and fixed principal value.

LPL Tracking #1121474